Fraud Risk Management: Types, Frameworks & Best Practices

- Posted by GRMI

- Categories Blog, pgdrm blog

- Date June 11, 2026

Fraud Risk Management: Types, Frameworks & Best Practices

Jump to ↓

Author: Jayant palan

Fraud can expose organisations to financial losses, regulatory penalties, and reputational damage. This guide explores fraud risk management, common fraud risks, assessment processes, key frameworks, and best practices for building a strong fraud risk management programme.

Fraud Risk Management: A Practical Guide for Risk Managers

Most organisations do not expect fraud to become a major issue until an incident occurs. Yet fraud rarely appears without warning. In many cases, it develops through weak controls, inadequate oversight, process gaps, or opportunities that remain unnoticed over time.

Whether it involves employee misconduct, procurement irregularities, payment fraud, or financial manipulation, fraud can have consequences that extend far beyond financial losses. Regulatory scrutiny, reputational damage, operational disruption, and a loss of stakeholder trust often follow.

This is why fraud risk management has become an essential part of modern business governance. Rather than focusing solely on investigating incidents after they occur, organisations are increasingly adopting proactive approaches that help identify vulnerabilities, strengthen controls, and reduce the likelihood of fraud before it happens.

What is Fraud Risk Management?

Fraud risk management is the process of identifying, assessing, preventing, detecting, and responding to fraud risks that may affect an organisation.

It combines governance, internal controls, risk assessment, monitoring mechanisms, and response procedures to help organisations protect their assets, people, and reputation.

An effective fraud risk management programme recognises that no organisation is completely immune to fraud. The objective is therefore to minimise opportunities for fraud, improve early detection capabilities, and ensure an effective response when incidents occur.

Importantly, fraud risk management is not solely the responsibility of internal audit or compliance teams. It requires involvement from leadership, business functions, risk teams, and employees across the organisation.

Why Fraud Risk Management Matters for Your Organisation

Fraud risks continue to evolve alongside changing business models, digital technologies, and increasingly complex supply chains.

Without a structured approach to fraud risk management, organisations may face:

- Direct financial losses

- Regulatory fines and penalties

- Legal disputes

- Reputational damage

- Loss of customer confidence

- Business disruption

In highly regulated sectors such as banking, financial services, insurance, and healthcare, fraud incidents can also attract significant scrutiny from regulators and stakeholders.

A proactive fraud risk management programme enables organisations to identify weaknesses before they are exploited and strengthen resilience against both internal and external threats.

Common Types of Fraud Risk

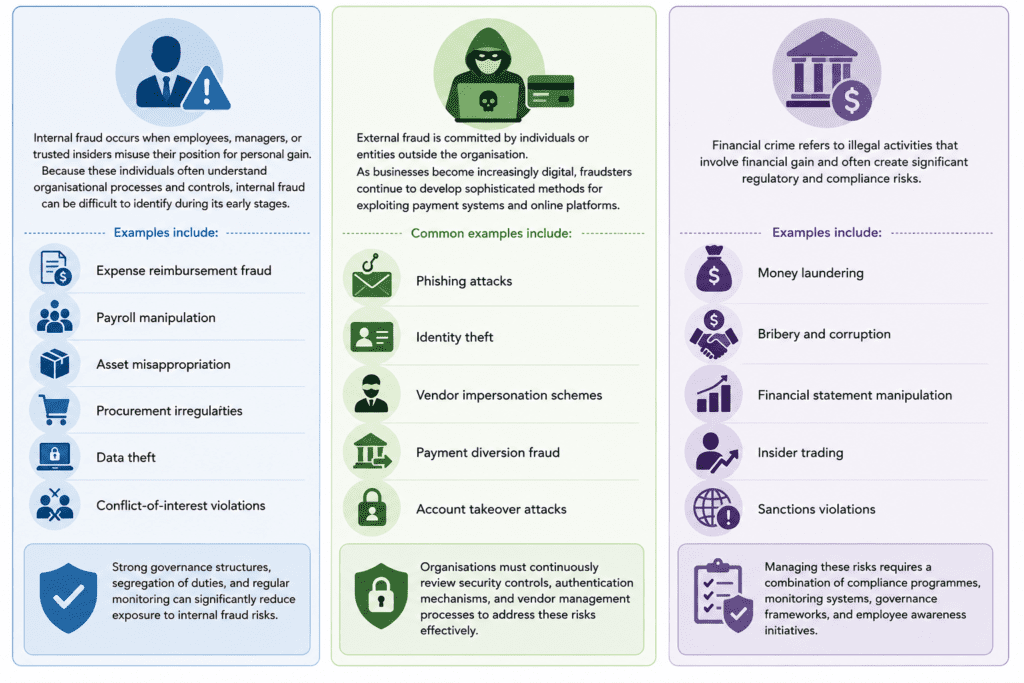

Internal Fraud and Employee Misconduct

Internal fraud occurs when employees, managers, or trusted insiders misuse their position for personal gain.

Because these individuals often understand organisational processes and controls, internal fraud can be difficult to identify during its early stages.

Examples include:

- Expense reimbursement fraud

- Payroll manipulation

- Asset misappropriation

- Procurement irregularities

- Data theft

- Conflict-of-interest violations

Strong governance structures, segregation of duties, and regular monitoring can significantly reduce exposure to internal fraud risks.

External Fraud and Payment Fraud

External fraud is committed by individuals or entities outside the organisation.

As businesses become increasingly digital, fraudsters continue to develop sophisticated methods for exploiting payment systems and online platforms.

Common examples include:

- Phishing attacks

- Identity theft

- Vendor impersonation schemes

- Payment diversion fraud

- Account takeover attacks

Organisations must continuously review security controls, authentication mechanisms, and vendor management processes to address these risks effectively.

Financial Crime

Financial crime refers to illegal activities that involve financial gain and often create significant regulatory and compliance risks.

Examples include:

- Money laundering

- Bribery and corruption

- Financial statement manipulation

- Insider trading

- Sanctions violations

Managing these risks requires a combination of compliance programmes, monitoring systems, governance frameworks, and employee awareness initiatives.

Fraud Risk Management Frameworks

A successful fraud risk management programme does not operate in isolation. Instead, it forms part of a broader risk management and governance framework.

Many organisations align fraud risk management with enterprise risk management principles to ensure fraud risks are considered alongside strategic, operational, financial, and compliance risks.

Effective frameworks typically focus on:

- Governance and accountability

- Fraud risk assessment

- Preventive controls

- Detection mechanisms

- Incident response procedures

- Continuous monitoring and improvement

By embedding fraud risk considerations into business operations, organisations can move from reactive responses towards proactive risk management.

How to Conduct a Fraud Risk Assessment

A fraud risk assessment helps organisations understand where they are most vulnerable and how effectively existing controls are managing those risks.

Step 1: Identify and Document Fraud Risks

The first step involves identifying potential fraud scenarios that could affect the organisation.

This typically includes reviewing:

- Business processes

- Financial transactions

- Procurement activities

- Third-party relationships

- Technology systems

- Regulatory obligations

Risk managers work with stakeholders to document possible fraud schemes and understand where vulnerabilities may exist.

Step 2: Analyse and Prioritise Fraud Risk Exposure

Not all fraud risks carry the same level of impact.

Once risks have been identified, organisations assess:

- Likelihood of occurrence

- Potential financial impact

- Reputational consequences

- Regulatory implications

- Operational disruption

This process helps prioritise resources towards the most significant risks.

Step 3: Develop, Implement, and Monitor Controls

After evaluating risks, organisations establish controls designed to reduce exposure.

Examples include:

- Segregation of duties

- Approval workflows

- Access management controls

- Transaction monitoring

- Vendor due diligence

- Whistleblowing mechanisms

Regular reviews ensure that controls remain effective as business activities and risk environments evolve.

Key Components of a Fraud Risk Management Programme

Fraud Risk Management Policy

A formal fraud risk management policy establishes expectations regarding ethical conduct, fraud prevention, reporting procedures, and accountability.

Clear policies provide consistency across the organisation and reinforce management’s commitment to ethical business practices.

Key Risk Indicators (KRIs) and Board Reporting

Many organisations use Key Risk Indicators (KRIs) to monitor potential fraud exposures and identify emerging concerns.

Examples may include:

- Unusual transaction patterns

- Control override incidents

- Vendor concentration levels

- Employee misconduct reports

- Compliance breaches

Regular reporting enables leadership teams and boards to maintain visibility over fraud-related risks and control effectiveness.

Fraud Incident Response Planning

Even the strongest controls cannot eliminate fraud risk entirely.

An effective incident response plan helps organisations:

- Investigate allegations efficiently

- Preserve evidence

- Manage stakeholder communication

- Meet regulatory reporting requirements

- Implement corrective actions

Preparedness often determines how successfully an organisation can contain the impact of a fraud event.

Why Fraud Risk Skills Are Becoming Increasingly Important

As organisations strengthen governance and risk management practices, the demand for professionals with expertise in fraud risk, internal controls, compliance, and operational risk continues to grow.

Today’s risk professionals are expected to understand not only how fraud occurs but also how business processes, governance structures, and organisational culture influence fraud exposure.

This broader perspective allows organisations to move beyond detection and build stronger prevention capabilities.

Practical Case Studies and Industry Examples

Fraud risk becomes much easier to understand when we look at how it has actually played out in real organisations. In most cases, fraud does not happen suddenly. It builds up quietly through gaps in controls, pressure in the system, or weak oversight that goes unnoticed until the impact becomes significant.

A well-known case from the Indian IT sector

A widely discussed example is the situation involving Satyam Computer Services.

The company’s financial statements were found to be significantly overstated over a period of time. What makes this case important from a risk perspective is not just the fraud itself, but how it remained undetected for so long.

In hindsight, the gaps were clear—limited oversight, weak internal checks, and over-reliance on reported numbers without deeper validation.

What this teaches us: Even strong organisations can face serious fraud risk when governance and independent monitoring are not strong enough.

When internal pressure turns into misconduct

The case of Wells Fargo is often cited when discussing internal fraud and conduct risk.

Employees were found to have created unauthorised customer accounts in order to meet aggressive sales targets. While systems and policies existed, the real issue came from the pressure of performance expectations and incentive-driven behaviour.

What this teaches us: Fraud risk is not only about controls on paper. It is also shaped by workplace culture, incentives, and how performance is measured.

Digital payments and email impersonation fraud

In recent years, many organisations across industries have reported losses due to business email compromise (BEC) attacks.

In such cases, fraudsters impersonate senior executives or trusted vendors and request urgent fund transfers or changes in bank details. These requests often appear legitimate and are acted upon without proper verification.

What this teaches us: In digital environments, even a small lapse in verification can lead to significant financial loss. Strong approval workflows and verification steps are essential.

What these cases really show

When you look at these examples together, one thing becomes clear—fraud rarely happens because of a single mistake.

It usually develops through a combination of:

- Weak oversight

- Gaps in internal controls

- Pressure-driven environments

- Lack of verification at key steps

- Limited risk awareness across teams

This is why organisations today focus more on building proactive fraud risk management systems rather than reacting after something goes wrong.

Ultimately, the goal is simple: identify risks early, strengthen controls, and create an environment where fraud has fewer opportunities to exist.

Develop Effective Fraud Risk Management Plans with GRMI

Effective fraud risk management requires more than investigative skills. It requires an understanding of risk assessment, governance frameworks, internal controls, compliance requirements, and business operations.

For individuals seeking to build expertise in these areas, specialised risk management education can provide a strong foundation.

The 1-year Post Graduate Diploma in Risk Management (PGDRM) offered by GRMI is designed to help students understand how organisations identify, assess, monitor, and mitigate a wide range of risks, including fraud-related risks.

The programme provides exposure to areas such as:

- Enterprise Risk Management

- Operational Risk Management

- Governance and Compliance

- Internal Control Frameworks

- Regulatory Risk

- Business Continuity and Resilience

- Risk Analytics

By combining theoretical concepts with practical business applications, the programme helps students develop skills that are increasingly relevant across consulting firms, financial institutions, corporate risk functions, and advisory organisations.

Conclusion

Fraud risk management is no longer viewed as a standalone compliance activity. It has become a critical business function that supports organisational resilience, protects stakeholder interests, and strengthens governance.

Organisations that proactively identify fraud risks, implement effective controls, and foster a culture of accountability are better positioned to manage uncertainty and respond to emerging threats.

As fraud risks continue to evolve, a structured and forward-looking approach to fraud risk management will remain essential for long-term business success.

FAQ's

Fraud risk management is the process of identifying, assessing, preventing, detecting, and responding to fraud risks that may impact an organisation.

It helps organisations reduce financial losses, strengthen governance, improve compliance, and protect their reputation from fraud-related incidents.

Common fraud risks include internal fraud, employee misconduct, payment fraud, procurement fraud, financial statement fraud, and various forms of financial crime.

A fraud risk assessment is a structured process used to identify potential fraud risks, evaluate their impact, and determine whether existing controls are sufficient.

KRIs are measurable indicators used to monitor risk exposure and provide early warning signs of potential fraud or control weaknesses.

Professionals can develop fraud risk management capabilities through practical experience, industry certifications, and specialised programmes that focus on risk management, governance, compliance, and internal controls.